Mood in Munich buoyant despite falling rates

Supply chains changing, e-commerce set for further growth, but SAF far from the complete solution on sustainability

Supply chains changing, e-commerce set for further growth, but SAF far from the complete solution on sustainability

But if China keeps growing fast and any recession in the West is brief and shallow, perhaps the market may yet reach a bottom soon

The collapse of Silicon Valley Bank and last-ditch rescue of Credit Suisse have raised the spectre of a renewed financial crisis. But this time does look a bit different.

Lower energy prices and cargo rates may lead to a soft landing for the world economy – and a quicker rebound

The global economy has been stalling – and air freight prices falling. After a big surge during Covid, is the market dropping back as far as pre-pandemic levels?

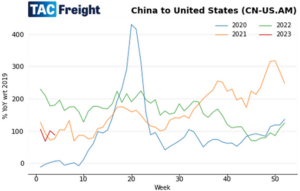

Shippers and carriers are looking increasingly towards index-linked agreements (ILAs) to manage price volatility.

Following a massive surge during the Covid-19 pandemic years, air freight prices have been trending a long way back down over recent months. According to the latest data from TAC Index, the leading price reporting agency (PRA) for air freight, the overall Baltic Air Freight Index (BAI00) is now down a massive -41.3% in the 12 months to 28 November – though still remains, so far, comfortably above pre-pandemic levels. During the past year, there have been some notable regional variations – with routes from China more hard hit than from other major locations, with the index for Outbound Shanghai routes (BAI80) down more steeply by -52.5% YoY. In parts of Southeast Asia, the drops have been more extreme with Vietnam to US and Vietnam to Europe routes, which are dominated more by spot market activity than bigger markets like Shanghai and Hong Kong, both down more than -70% YoY according to the latest TAC data. Over the same period, prices have held up more strongly out of Europe, with the Outbound Frankfurt index (BAI20) only down by -26.4% YoY. And out of North America, the Outbound Chicago index (BAI50) is only down -27.1% YoY. Over the same period, US to Europe routes are only down -7.6%. And US to South America routes are also less negatively affected, with Miami to South America only down -8.7% YoY. So there has been plenty of regional variation. But the overall narrative has been pretty consistent – and consistently bad given negative factors like: These developments have also come at a time when more air freight capacity has been coming back on stream following the pandemic – making more planes available to move less goods. And following a general move by shippers away from ‘just in time’ and towards ‘just in case’ supply chain systems – which has meant inventories high and warehouses full – at a time economic activity has been stalling. All of which leading of course to lower rates for air freight. But, despite the negativity, could all that be about to change? Could the tide turn – and we suddenly reach an inflection point? Over the past month or so, there have been some signs such a change of direction may be coming. First of all, there has been a collapse in European gas prices – arriving like manna from heaven for governments in Europe and the UK, who had been forced into massive support packages to shelter households and businesses from soaring gas and electricity prices. Big support packages for the winter of 2022-23 are already in place. But this recent drop in gas prices should much reduce the level of support required for the following period. That in turn seems to have eased the most gloomy scenarios of a major recession in Europe – boosted by a feeling that Ukraine has now gained the upper hand over Russia, which may help end the war there more swiftly. Second, expectations of rising inflation in the US – which had been causing alarm for markets all around the world – appear to be approaching a peak. With the latest US inflation figures coming in below expectations, markets now expect Federal Reserve chairman Jerome Powell to have more leeway not to push interest rates so high – and hence not squeeze so much growth out of the global economy. Third, and perhaps most importantly, have been expectations that a full reopening of China – post-Covid – must finally happen, and perhaps soon. All of this has been reflected in a sudden surge in global equity prices over the past couple of months, with the MSCI World up more than 6% in November as we approached month-end – and more than 10% in European markets, buoyed by that falling gas price. Taken together, these developments have raised expectations that although the global economy may still be heading for recession, it could be with more of a ‘soft landing’ – which might also mean the ongoing fall in air freight prices coming to an end. Against that, it must be said that plenty of economists and macro commentators remain sceptical that a soft landing can indeed be achieved. Some of these sceptics view the recent equity market rise as something of a ‘dead cat bounce’ – the kind of short term relief rally that often occurs in a bear market. They point to various things – not least that the Ukraine conflict remains far from over, ongoing trade tensions between the US and China, and what they see as a disappointing outcome at the recent Chinese Party Congress – all as factors of concern. The more recent outbreak of nationwide protests across China against continuing Covid restrictions – and market reaction in Asia – will not have eased such concerns. With supply chains in China far from back to normal, there is clearly still plenty to beconcerned about. But it could be that an inflection point is coming. Even if so, an end to the long running fall in air freight prices may take a while to show through – perhaps not until next March or April at the soonest. Any sign of it before then would indeed be an early indicator.

During the recent IATA World Cargo Symposium, held in London in late September, you could almost feel a palpable sense of pride in the industry. After all, despite falls this year in air freight price levels as measured by Price Reporting Agency (PRA) TAC Index, the sector had undoubtedly proved its importance to the whole world during the years of the Covid pandemic. Without the ability to fly vast quantities of personal protective equipment (PPE) and key pharmaceuticals, the amazingly rapid global vaccine rollout in response to Covid would simply not have been possible. Yet the very importance of the air freight sector still comes across as something of a surprise even within the aviation industry itself. Ross Baker, chief commercial officer at London Heathrow, caused some gasps in the audience at IATA when he noted, for instance, how an incredible one-third of all UK cargo – by value – had gone through Heathrow in 2019, weighing in at a cool £140 billion that year. The cargo side of aviation – by common consent – had in previous times always been something of an after-thought as compared with the bigger, more glamorous, and more profitable air passenger traffic business. Covid, of course, put a virtual halt to passenger traffic – and at a stroke simultaneously elevated the importance of freight. Air cargo had not been seen in the past as such a priority at Heathrow, Baker admitted. Post-Covid, that was now emphatically no longer the case. Nevertheless, the air cargo sector still faces some powerful and severe challenges and headwinds – including not least due to continuing perceptions and concerns about its environmental footprint, and negative image as a sector in which to forge a career. Brendan Sullivan, global head of cargo at IATA, trumpeted the progress the industry was making towards a goal of net zero carbon emissions by 2050 – and the key role to be played by sustainable air fuel (SAF) in achieving that. But other participants at the conference were more sceptical, with some noting there had been plenty of talk about SAF and cutting carbon for a number of years – and not much progress yet. Jonathan Wood, VP in renewable aviation at Neste, noted how SAF was still generally much more expensive than jet fuel even at a time when oil prices were high and the ‘crack spread’ – the relative price of jet fuel to crude oil – was elevated, as noted by IATA chief economist Marie Owens-Thomsen. Martin Drew, senior VP for cargo at Etihad, also noted a continuing lack of alignment and consistency of regulatory treatment for SAF around the world – with an outlier like the state of California offering subsidies, but in other places SAF being up to eight times the price of jet fuel. There are various initiatives by air freight carriers now in progress towards cutting carbon emissions and steadily using more SAF. But the patchy progress overall so far is no doubt one of various factors that makes air cargo be seen as an undesirable sector in which to work. Indeed, there was a sobering presentation at the Symposium from Arpad Szakal, a principal consultant on recruitment at Cormis Partners, on the challenges to recruiting and retaining talent in the sector. After many airlines had cut both the number of staff and working conditions aggressively during the pandemic, the whole aviation sector now faced a problem in human resources, Szakal noted. This could be seen all too readily on the passenger traffic side – with a lack of sufficient check-in and baggage handling staff feeding through to large numbers of flight cancellations. On the cargo side, there were also perceptions in the workforce of an industry of mostly low skilled work – with jobs packing and shifting boxes – making it hard to attract talented people, and especially females, Szakal noted. Research showed that some two-thirds of companies operating in air cargo were now under-staffed, with a shocking staff turnover in the first year of 40%-plus in many companies, he claimed. Moreover, pay and prospects were not seen to be good or competitive with other sectors at all levels up the corporate scale – not just at entry level, Szakal added. Of course, there are ways to remedy these perceptions – with pro-active approaches on incentives, retention, diversity and inclusion, ‘reskilling’ and ‘upskilling.’ But the central point surely is to emphasise the ongoing importance of the sector – which is surely going nowhere soon given its key role in the global economy, especially if progress on carbon and SAF can be accelerated. With this in mind, it is interesting to note that after trending down in recent months, air freight prices have firmed up recently – with the overall Baltic Air Freight Index (BAI00) up +4.9% in the week to 24 October as the long-awaited ‘peak season’ ahead of the US Thanksgiving holiday finally approached. Though still down -28.5% year-on-year amid a murky macroeconomic outlook, air freight prices overall remain well above pre-pandemic levels. The ongoing importance of the industry to the global economy simply cannot be denied.

Gas prices in Europe skyrocketing. Lockdowns in China lingering. Russia losing ground but now seeking to annexe chunks of Ukraine. Countries like the UK responding with huge subsidies for energy consumers – and large tax cuts to boot – massively increasing their fiscal deficits, and shaking the confidence of markets. Central banks also responding – not with more monetary largesse this time, but with interest rates rising sharply. Nevertheless, still leaving a serious threat of inflation running out of control. And how is all this being reflected in air freight markets – often a leading indicator for the global economic outlook? Well, the air cargo sector is certainly looking a little edgy and nervous. Prices have been slipping for a while, with the overall Baltic Air Freight Index (BAI00) – calculated by TAC Index – now down by some -24.5% year-on-year to 26 September, after another drop of -5.3% in the latest week. Normally, at this time of year, prices tend firm up – as the air freight sector gears up for peak season, when demand traditionally rises in the run up to Thanksgiving, Black Friday, Christmas and New Year. But this year, prices have not been rising but slipping for many weeks. And even a recent rise in the previous week, sources suggested, tended to reflect longer term contracts – prevalent on many of the major routes – rather than spot prices, which were continuing to trend lower. The Baltic air freight indices for almost all of the major outbound locations fell on the latest weekly data – with Shanghai (BAI80) down -8.4% WoW, Hong Kong (BAI30) falling -1.9%, Frankfurt (BAI20) down -3.9% and Chicago (BAI50) off a steep -17.7%. London (BAI40) was the one exception with a modest gain +3.0%. But price trends out of other locations, where more of the market is conducted at spot rates, were more mixed. India to US routes, for instance, fell -4.0% on the latest week – leaving them languishing by -33.3% YoY, a bigger drop than on the Baltic BAI00 index. Vietnam to US routes, on the other hand, did gain a modest +2.9% WoW – but the YoY decline on those routes was still looking very steep at -40.3%. Earlier in the year, when air freight prices were still high or rising, many market watchers had been expecting to see the very opposite of those trends. With local lockdowns – and Covid policies – continuing to disrupt supply chains from important manufacturing centres like Shanghai and Shenzhen, many had expected business to move where possible via other locations such as Vietnam. But that doesn’t seem to have happened – certainly not to much of an extent. And it is indeed a murky outlook ahead – as the recent Q1 results from FedEx, which surprised the market, arguably underlined. FedEx announced a miss on projected earnings of some $500 million – widely described as ‘of epic proportions’ – with the company issuing a profit warning that slashed its share price by more than -21% in a single day. Industry observers pointed to various factors – not least a loss of business due to disintermediation caused by other players such as Amazon taking business away – for the troubles at FedEx. But the weaker recent market will surely not have been helping, with FedEx CEO Raj Subramaniam forced to respond with an urgent plan to introduce cost savings going forward. To be fair, the market does present a complicated picture – as highlighted by Marie-Christina Lombard, CEO of Geodis, when presenting her company’s first-half results in September. Reflecting on what had been a period of strong growth in the first half for Geodis in terms of both revenues and profits, Lombard also highlighted that rates had already been falling in recent months for air freight as well as for ocean traffic. That said, there were some areas where demand remained strong – notably in the automotive sector, according to Lombard. And although e-commerce sector volumes had been weaker than expected, she still expected some uptick to be coming as usually happens by Q4. That may yet pan out, but it seems highly likely to be a bumpy ride ahead. Read our freight blog for the latest insights and trends in the logistics industry.

Whither air cargo rates – which way are they set to go? Are they set to rise as we reach the traditional peak season? Or are they set to crumble and fall – as rising fears about inflation and recession hit global trade?