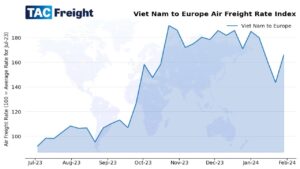

Markets spooked by carry trade worries and Temu results, but air freight rates stay firm

Air freight rates maintained a firm tone again through the month of August. The Baltic Air Freight Index (BAI00) gained another +5.6% over the four weeks to September 2, taking its rise over 12 months to +17.2%. Overall, rates have remained unusually strong throughout the summer – a season when they typically ease lower as higher passenger traffic adds extra bellyhold capacity. Market participants point to two factors in particular driving this year’s stronger price pattern: disruption to ocean traffic in the Red Sea – which has led to big delays and price hikes in ocean shipping; and the continuing rise of e-commerce, notably out of Asia. The rise of e-commerce has been reflected in the data out of China all year, and the index of outbound routes from Hong Kong (BAI30) was up a further +3.0% MoM taking its gain over 12 months to +25.0%. The outbound Shanghai index (BAI80) gained +7.8% MoM to put it ahead by an even more impressive +39.5% YoY. The rates on some other big lanes out of Asia, such as from India and Vietnam, have risen even more strongly over the past year. Indeed, rates out of Vietnam overall reached levels exceeding those from China. In August, however, rate rises from other regions were no longer lagging. Out of Europe, the index of outbound routes from Frankfurt (BAI20) was up +8.5% MoM to trim its YoY fall to only -10.1%. Outbound London Heathrow (BAI40) gained a chunky +10.4% MoM, cutting its YoY decline to only -7.6%. From the Americas, the index of outbound routes from Chicago (BAI50) gained a more modest +3.9% MoM – to show a YoY decline of -14.6%. Over the month, there was certainly a lot of ‘noise’ in the global macro outlook. Equity markets took a sharp tumble in early August amid rising fears of recession in the US – before recovering rapidly back towards previous highs. As the month came to a close, the S&P 500 index for instance was still up more than +25% YoY. The sharp fall in early August, however, was particularly steep in Japan where the Nikkei 225 index plummeted some -12% in only one day – its worst single day drop for many years. With interest rates finally rising in Japan, the equity market was suddenly gripped by worries local exporters would get hurt by a rising yen. There were also concerns about an end to the so-called ‘carry trade’ – whereby many investors all around the world have borrowed in yen for years virtually interest-free in order to invest in higher-yielding (and riskier) assets. Even though the move to higher rates had been well-signalled by the Bank of Japan, the sudden reality of a higher yen seemed to take many by surprise. Labour market and other data from the US subsequently calmed the jitters – plus expectations of faster and steeper interest rate cuts from the Federal Reserve and other central banks. As August came to a close, even the Nikkei 225 was back up over +18% YoY. Over the same period, there was the emergence of what some dub the ‘Trump trade’. This is based on expectations higher tariffs on imports to the US might in turn hit US exporters, including big tech companies that dominate the Nasdaq index – but benefit domestic companies that feature more in the Russell 2000 index. Needless to say, the relative performance of the Nasdaq and the Russell waxed and waned as odds on a Donald Trump victory in the US Presidential election first increased and then reduced – after Kamala Harris was chosen to replace Joe Biden as the Democratic Party candidate. Companies that export a lot to the US – particularly from China, though also to some extent from Europe – are certainly concerned about prospects for higher tariffs and/or other new barriers to trade. As noted previously, however, it seems strange markets are so worried about Trump – given that the Democrats, under Biden, have proved pretty much as hawkish on trade issues. Under Biden, the US has not removed but added to tariffs introduced by Trump. It has also passed the misleadingly titled Inflation Reduction Act (IRA), designed in part to incentivise developments to address the climate transition, but which some critics view as the most protectionist piece of legislation in US history. Prospects for higher tariffs and other barriers to trade with the US – and also with the EU – are not coming at a great time for China. After an initial rebound last year when Covid restrictions were eased, the Chinese economy has since got mired in a construction and property sector crisis – with consumers responding by cutting spending and increasing (already high) savings levels. The resulting decline in growth and economic activity has arguably exacerbated other knock-on effects, including a rise in youth unemployment. Hitherto, one bright spot for China has been the e-commerce sector –driven both domestically and internationally by the increasing popularity of cheaper non-branded goods. While volumes of other goods are probably little changed this year, it has been the rise in e-commerce that has lifted activity and average rates in air freight overall. In late August, however, even the seemingly unstoppable rise of e-commerce was coming into doubt – as leading player Temu delivered a set of results that surprised and disappointed the market with lower than expected levels of growth. The share price of Temu parent company, PDD Holdings, fell sharply after the results were announced – alongside some words of caution about the outlook from CEO Chen Lei. Perhaps, as with the sudden fall in the Nikkei, this sudden drop in PDD shares may come to be seen as an over-reaction by the market. After all, Temu revenues were still up some +86% from the previous year, and with a profit margin actually ahead of expectations – not dissimilar to the performance of AI giant Nvidia, which also disappointed market expectations despite huge growth. The rate of growth at